Off-Plan Payment Plans in Dubai

Off-Plan Payment Plans in Dubai: Why Smart Investors Should Compare Them in Today’s Money.

By Gareth Davies, Award-Winning Property Consultant.

A Dubai off-plan payment plan can look attractive on paper simply because the cash leaves your bank account later. But from an investment perspective, the real question is not only how much you pay. It is also when you pay it. That is exactly where discounted cash-flow analysis, or DCF, becomes useful. Finance theory treats value as the present value of future cash flows, and it also makes the basic point that cash flows received or paid at different times cannot be compared properly until they are brought back to the same point in time. (CFA Institute)

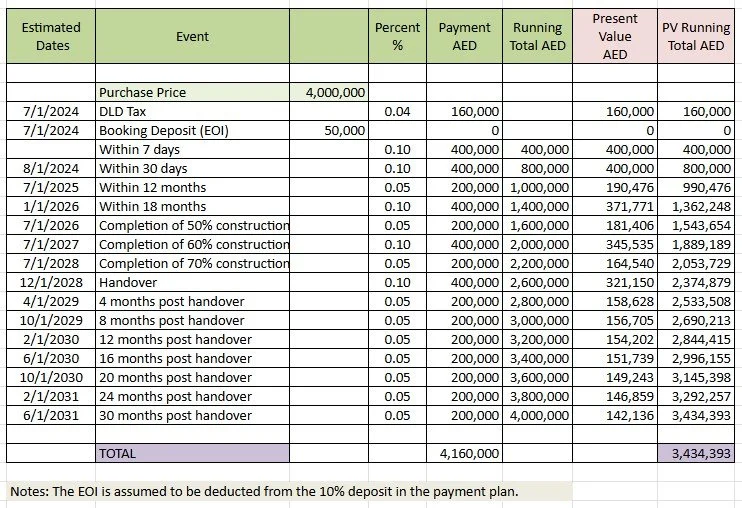

The discount cash-flow analysis shown below was for a post-handover payment plan I carried out in JVC Dubai.

DCF Appraisal carried out by Gareth Davies

In simple language, DCF converts future payments into today’s money. The logic is straightforward: a dirham paid three years from now is not economically the same as a dirham paid today, because money has a time value. The discount rate reflects that trade-off and incorporates opportunity cost, inflation expectations, and risk. A higher discount rate reduces the present value of future cash flows. (CFA Institute)

That matters in Dubai’s off-plan market because developers do not all use the same structure. Some projects are sold on more traditional schedules such as 80/20, where most of the price is paid during construction and the final portion on handover. Emaar’s buyer guidance, for example, describes an 80/20 structure with the last 20% payable at handover, while Emaar project material also shows examples of 60/40 payment plans. At the same time, some developers market post-handover structures in which part of the balance remains payable after the keys are received. DAMAC’s own payment-plan guidance describes a “60/40 with post-handover” structure in which 60% is paid before handover and the remaining 40% is paid over one to three years after handover. (Emaar Properties)

This is why headline price alone can be misleading. Two units may both be advertised at AED 2 million, but one may require a large final payment at handover while the other allows the same balance to be paid over the next two or three years. Nominally, the price is the same. Economically, the cash burden is not. DCF helps an investor compare those alternatives on a like-for-like basis. (CFA Institute)

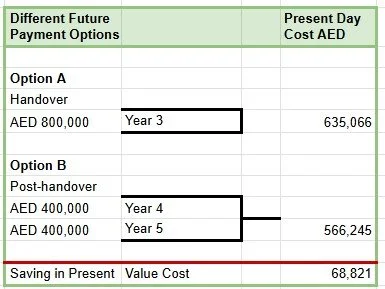

Take a simple illustration. Assume the purchase price is AED 2,000,000, and the first 60% of the price is identical under both plans during construction. The only difference is the final 40%, equal to AED 800,000. Under Plan A, that AED 800,000 is payable on handover at the end of year 3. Under Plan B, it is payable as AED 400,000 at the end of year 4 and AED 400,000 at the end of year 5 under a post-handover plan. If the investor uses an 8% discount rate, the present value of AED 800,000 payable in year 3 is about AED 635,066. By contrast, the present value of AED 400,000 in year 4 plus AED 400,000 in year 5 is about AED 566,245. In this simplified example, merely deferring the same nominal 40% reduces its present-value cost by roughly AED 68,821.

That does not mean the second plan is always “better.” It means the later payment profile is economically lighter in today’s money, assuming the sticker price is the same and the risk is acceptable. If the developer charges a premium for the longer payment plan, that premium should also be brought into the DCF. A plan that looks flexible can still be expensive if the launch price is inflated to compensate for that flexibility. The proper comparison is therefore not only price versus price, but present value versus present value. (CFA Institute)

Where the analysis becomes especially interesting is with post-handover payment plans. Once the property is handed over, the owner can move into the operating phase of the asset rather than the construction phase. In Dubai, tenancy registration is handled through Ejari, and DLD’s systems allow owners and tenants to register or renew tenancy contracts and manage leases through Dubai REST. DLD also states that Dubai REST gives owners information on items such as rental return and service charges. In practical investment terms, that means a landlord may be able to start generating rent after handover while still paying the remaining instalments under a post-handover schedule. (Dubai Land Department)

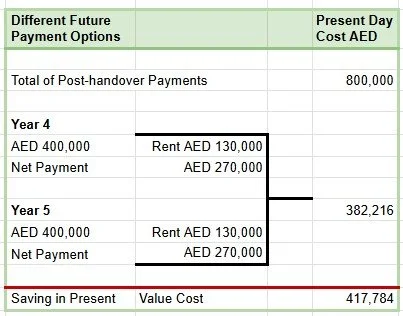

That rental stream can materially change the investor’s net cash burden. Suppose, in the same example above, the property produces AED 130,000 a year in net rent after allowing for normal operating leakage such as vacancy and property-level costs. If the post-handover balance is AED 400,000 in year 4 and AED 400,000 in year 5, that rent could reduce the owner’s out-of-pocket cash contribution to AED 270,000 in each of those two years. Discounted at 8%, those two net contributions have a present value of about AED 382,216. That is a very different cash profile from having to fund a full AED 800,000 on handover before the rental stream has had time to do any work.

This is the real financial significance of post-handover plans. They do not magically make a property cheap. What they may do is shift part of the burden from the investor’s own capital today to the asset’s income tomorrow. For a landlord, that can improve liquidity, reduce immediate equity strain, and sometimes make a marginal deal more manageable. Compared with a classic 60% during construction and 40% on handover structure, a post-handover plan often produces a softer DCF profile because more of the payment is pushed into later years and, potentially, partly serviced by rent.

However, investors should not treat this as an automatic win. DCF is only as good as its assumptions. A weak rental market, handover delays, snagging issues, a longer leasing-up period, service charges, furnishing costs, or a higher required return can all reduce the apparent advantage. In addition, the mechanics of post-handover plans matter. Emaar’s own finance fact sheet states that for a post-handover payment plan, the owner must submit post-dated cheques for the remaining instalments at handover, and service fees must be paid before taking over the property. Those details affect cash planning and remind buyers that “deferred” does not mean “cost-free.” (Emaar Properties)

The wider lesson for Dubai off-plan investors is that payment-plan structure is part of valuation. A broker, investor or buyer who looks only at brochure price may miss the economic picture. DCF gives a more disciplined way to compare a traditional handover-heavy structure with a post-handover plan by translating both into today’s money. For end-users, that can help with affordability planning. For landlords, it can help assess whether future rental income is likely to support the tail end of the plan. For investors, it is often the difference between analysing a deal properly and simply reacting to marketing language.

In short, off-plan payment plans should be treated not just as sales incentives, but as cash-flow structures. And once you analyse them that way, you often see that two deals with the same headline price do not have the same economic cost at all.

References

CFA Institute, Free Cash Flow Valuation and Time Value of Money in Finance. (CFA Institute)

Aswath Damodaran, NYU Stern, Session 6: The Time Value of Money. (pages.stern.nyu.edu)

Emaar Properties, First-Time Home Buyer Guide in Dubai and Address Grand Downtown project page. (Emaar Properties)

DAMAC, Installment Plans in Dubai. (damacproperties.com)

Dubai Land Department, Register / Renew Rental Contract and Dubai REST. (Dubai Land Department)

Emaar Properties, Finance Department Fact Sheet. (Emaar Properties)

Disclaimer: This article is a general educational guide only. It is not investment advice, legal advice, tax advice, or a formal valuation. Any real appraisal of an off-plan deal should consider the exact SPA terms, service charges, fit-out costs, vacancy assumptions, financing costs, handover timing, rental risk, and default provisions. Where there are serious contractual or legal concerns, a qualified UAE real estate lawyer should be consulted, and where substantial capital is at stake, independent financial or valuation advice should also be obtained.

Ready to Find Your Dream Property in Dubai?

Get Expert Guidance & Personalized Investment Advice

Connect with me directly on WhatsApp for: